Business spotlight: San Miguel Corporation

Providing vital goods and services, serving human dignity and the common good, and creating value for all stakeholders

In 1890, when the Philippines was a Spanish colony, Southeast Asia’s first brewery, La Fábrica de Cerveza de San Miguel, produced and bottled what would eventually become one of the best-selling beers in the region, and among the top beer brands in the world — San Miguel Beer.

San Miguel Beer was my first beer. It was a right of passage. It became part of my celebrations with family and friends. It is a staple in every restaurant, bar, and far-flung sari-sari store (neighborhood micro-convenience store).

My investing education began with San Miguel in the early 1980s. Perhaps amused by my hallucinations as a young and aspiring Warren Buffett, a wise and older San Miguel senior executive, shareholder, and friend took pity and decided to tag me along with him to attend what would be my very first stockholders’ meeting. As we took our seats, he got hold of another copy of San Miguel’s annual report, handed it to me, and said, “Read this. It’s like a business manual. It’s required reading in the business schools.”

While a small army of lawyers were running up and down the aisles, spewing words of parliamentary procedure to waiting microphones, my attention turned toward an aristocratic-looking silver-haired gentleman seated on stage next to San Miguel’s chief executive. He had a double-breasted blue blazer draped over his shoulders. He was the spitting-image of Richard Chamberlain in The Count of Monte Cristo. He never said a word. He wasn’t asked a question. All he did was smile and wink repeatedly at a pair of giggling super models seated in the front row. I was later told by my wise and older companion that the gentleman was a major shareholder and descendant of one of San Miguel’s founders.

I’ve been following San Miguel’s progress ever since.

A collection of vital businesses

San Miguel Corporation (PSE: SMC) today engages in food and beverage, packaging, fuel and oil, energy, and infrastructure businesses worldwide.

Its mission and driving force is to lead efforts to deliver on national goals, setting the pace of progress in the Philippines, by providing goods and vital services well within the reach of every person, making their daily lives better and a celebration.

Its revenues of ₱1.02 trillion ($20.1 billion) in 2019 accounted for about 6% of the nation’s gross domestic product. In other words, the value of San Miguel’s goods and services, business investments, and exports, contributes greatly to the nation’s wealth.

Its Food and Beverage segment is involved in feeds production; poultry and livestock farming; processing and selling poultry and meat products; processing and marketing refrigerated processed and canned meat products; milling, manufacturing, and marketing flour, flour mixes, bakery ingredients, butter, margarine, cheese, milk, ice cream, jelly-based snacks and desserts, oils, salad aids, biscuits, and condiments; importing and marketing coffee and coffee-related products; and grain terminal handling. This segment also produces, markets, and sells beer and non-alcoholic beverages; and hard liquor in the form of gin, Chinese wine, brandy, rum, and vodka.

Its Packaging segment produces and markets packaging products, such as glass containers and molds, polyethylene terephthalate (PET) bottles and preforms, PET recycling, plastic and metal closures, corrugated cartons, woven polypropylene, kraft sacks and paperboards, pallets, flexible packaging, aluminum cans, woven products, industrial laminates, and radiant barriers, as well as plastic crates, floorings, films, trays, pails, and tubs. This segment also engages in the crate and plastic pallet leasing, PET bottle filling graphics design, packaging research and testing, packaging development and consultation, and contract packaging and trading activities.

Its Fuel and Oils segment, through Petron Corporation, is the market leader in the Philippine fuels and oils industry, and is a strong player in the Malaysian downstream oil market.

Its Energy segment generates, sells, retails, and distributes power. It has a full spectrum of three IPPA contracts and greenfield power plants. This segment’s portfolio has a combined capacity of 4,197 megawatts as of 2018, accounting for 25% of the Luzon grid, 9% of the Mindanao grid, and 19% of the national grid. (4,197 megawatts can power about four million and more homes per hour.)

Its Infrastructure segment develops, constructs, manages, and operates the nation’s largest infrastructure network of airports, roads, highways, toll roads, freeways, skyways, flyovers, viaducts, interchanges, and mass rail transit systems.

The company also provides banking services and develops, manages, and sells real estate properties.

Serving human dignity and the common good

San Miguel is guided by a strong sense of social, environmental, and economic responsibility.

BizNewsAsia chief executive and journalist, Tony Lopez, has been covering San Miguel and its chief executive, Ramon S. Ang, or RSA, in depth. In his April 9, 2021 Manila Standard column, Lopez wrote:

“SMC rejigged its liquor plants to produce alcohol. It gave away 1.6 million liters of alcohol free. It also gave away thousands of PPEs. It has ordered one million doses of various vaccines for its employees, their families, and to help poor families.

“Noticing the frequent flooding of Metro Manila, SMC is spending ₱2 billion of its own money to dredge the 18-km Pasig River to excavate, over the next five years, three million cubic meters of silt at the Manila side of the river, to increase the river’s carrying capacity from Laguna Bay to Manila Bay as well as drain waters from the rivers of Tullahan, Marikina, Manggahan, Meycauayan and Norzagaray, and the project will save taxpayers ₱200 billion a year in flood control.

“RSA plans to put up two large hospitals, one in south of Manila and another in the north. He will tie up with a large Manila university to build up a teaching force in medicine and nursing to man a school of medicine and a nursing school to support the south hospital. He wants to tie up with a leading US teaching and research institution to operate the Bulacan hospital and school of medicine adjacent to the ₱740 billion SMC Aerocity complex in Bulakan town.

“In the food business… it is farming out its piggery, turning up to 100,000 farmers into self-employed entrepreneurs. These farmers now grow the pigs, slaughter them, process them, freeze the parts and sell them to the company. Ang has lent capital, machinery and equipment, and built a slaughter house for the piggery farmers. Corn farmers, which produce the feeds for the pigs, have joined the enterprise.”

Creating value for all stakeholders

Does serving human dignity and the common good come at the expense of shareholder wealth creation?

A fundamental driver of a company’s value is its return on invested capital. It measures a company’s ability to create value for all its stakeholders: customers, suppliers, employees, the government (via taxes paid), debt providers, equity holders, and even society at large.

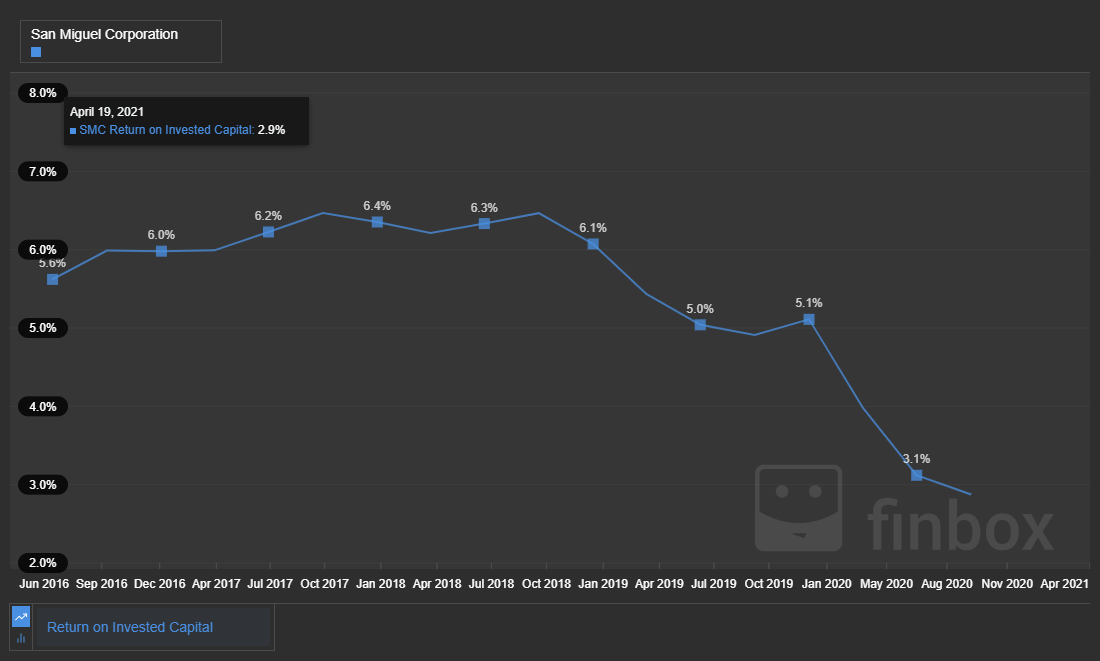

The following summarizes the trend and insights of San Miguel’s historic returns on invested capital:

San Miguel created value for all its stakeholders. Its returns on invested capital were positive and averaged 5.8% over the past five years.

However, its return on invested capital fell significantly from 5.1% in 2019 to 2.9% for the 12 months ended September 2020. The fall reflected the impact of the government’s quarantine restrictions, which affected the performance of the businesses in the first half of 2020. The decline in net operating profit after tax, or NOPAT, was caused mainly by the lower sales volume of Petron, and the beer and non-alcoholic beverages division under the food and beverage business, due to the implementation of lockdown and quarantine protocols. The impact was significant due to the volumes lost, the inventory losses incurred by Petron, the increase in alcohol tax, which took effect in January 2020, and the recurring fixed costs of the group, which continued during the quarantine period.

Despite the fall, San Miguel was still able to create value for all its stakeholders. Its return on invested capital of 2.9% in September 2020 was still above the Philippine industrial sector’s average return on invested capital of 1.8%. San Miguel outperformed 18 out of 29 conglomerates.

The following summarizes insights on San Miguel’s future net operating profits after tax:

Despite the fall in 2020, analysts forecast San Miguel's net operating profit after tax to grow to ₱51.5 billion in 2021 and to ₱65.7 billion by 2026.

In his same column, Lopez wrote that San Miguel’s chief executive is expecting better results:

“San Miguel… expects to generate ₱900 billion in revenues and ₱100 billion in profits this year. Revenues will be up 24% and operating profits up a hefty 40% over 2020’s ₱725.8 billion and ₱71.5 billion, respectively.”

If that happens, San Miguel’s future net operating profits after tax should be higher than what analysts predict, which should improve its returns on invested capital and create greater value.

Investment performance

San Miguel’s shares returned 18.5% (including dividends) over the past year and outperformed the Philippine stock market’s return of 16.3%.

Value estimates

Is San Miguel undervalued?

Market price: ₱117.00 (April 19, 2021)

Analysts’ target: ₱135.00

Average multiples valuation: ₱128.00

Conclusion

Shareholder wealth creation does not come at the expense of other stakeholders. Quite the opposite. Winning companies, like San Miguel, when compared to their competitors, have greater productivity, greater increases in shareholder wealth, higher employment, and are able serve human dignity and the common good.

Furthermore, the nation needs to support its companies if it wants to grow. San Miguel is 6% of the nation’s wealth. Studies have shown that a nation’s economic system based on maximizing shareholder value, accompanied by broad ownership of debt and equity, and an open market for corporate control, is closely linked with: a higher standard of living, greater overall productivity and competitiveness, and a better functioning equity market. If a nation’s economic system is not based on maximizing shareholder value, and gives investors lower returns on capital than other nations that do, it will slowly be starved for capital, as capital markets continue to globalize, and fall farther behind in global competition. A value-based system becomes ever more important as capital becomes ever more mobile.

The International Investor does not own shares of San Miguel Corporation and does not receive compensation. This article is excerpted, edited, and sourced from the most recent company filings, company website, analysts’ reports, and S&P Global Market Intelligence. The content is for general informational and entertainment purposes only and should not be construed as financial advice.