Investing in Asia's Data Center Boom: Capitalizing on Surging Demand Driven by AI and Cloud Services

How can investors capitalize on the Asian data center boom?

In the fast-evolving landscape of data infrastructure, Asia emerges as the new frontier for global investors targeting data centers. Notable players like KKR and Bain Capital are seizing opportunities arising from the region’s escalating computing and data storage needs, fueled by a surge in artificial intelligence (AI) applications, according to insights from Bloomberg.

Similar to the United States, Asia is experiencing a significant uptick in demand for data centers, spurred by industry giants like Amazon and Google expanding their cloud services. The recent wave of generative AI applications is amplifying data and capacity requirements, while the burgeoning population in the region further intensifies the need for advanced storage solutions.

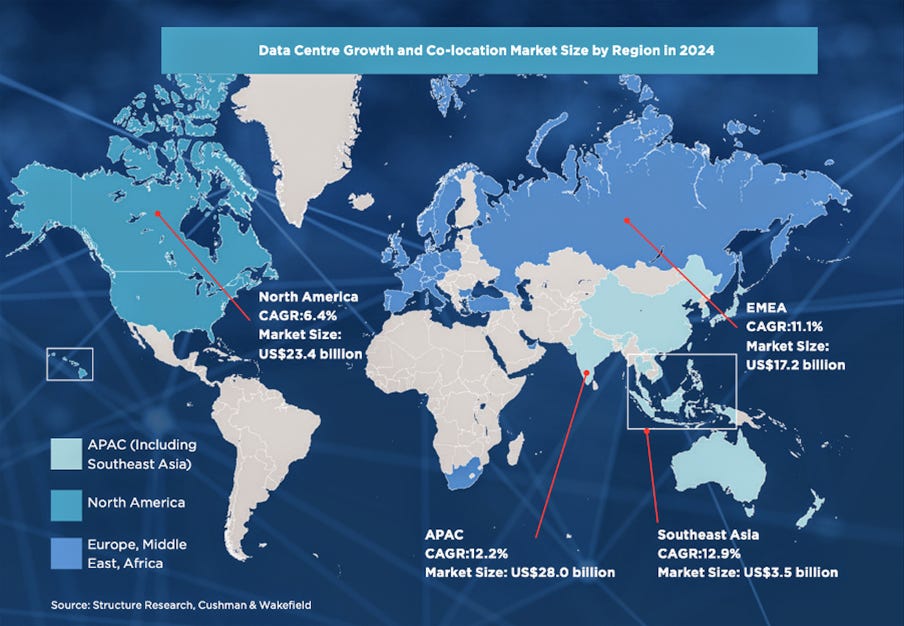

Projections from Cushman & Wakefield indicate a robust 25% annual growth in demand for data centers in Southeast Asia and North Asia through 2028, faster than their prior years’ 12% annual growth, and outpacing the 14% annual growth anticipated in the United States. Udhay Mathialagan, global head of Brookfield Asset Management’s data center business, notes that Asia, though diverse, shares a common trait — everyone is online, necessitating robust connectivity and high-quality data centers.

Investors are already making strategic moves. In August, Bain Capital announced a substantial deal to privatize Beijing-based Chindata Group Holdings with an implied equity value of US$3.2 billion. KKR followed suit in September by acquiring a 20% stake in Singapore Telecommunications’ regional data center business for approximately US$800 million. Blackstone also entered the arena, launching its wholly owned data center platform in Asia in November 2022.

Projesh Banerjea, Director of Infrastructure at KKR, envisions a potential investment of US$1 billion in equity for data center projects in the Asia-Pacific region in the coming years, with returns aligning with KKR’s infrastructure strategy targets in the mid-to-high teens.

The gamble lies in the expectation that Asia will carve out a larger share of the global data center market. Cushman & Wakefield forecasts that by 2028, Asia’s share of hyperscale cloud revenue — a proxy for market growth — could increase to 33%, amounting to $173 billion, up from the current 29%.

Morgan Laughlin, Global Head of Data Center Investments at PGIM Real Estate, emphasizes the simplicity of the investment story, citing relentless demand growth with no apparent endpoint and a constrained supply without a clear resolution in sight.

However, challenges abound. Developing data centers in Asia is a time-consuming and intricate process, demanding expertise in real estate, technology, local regulations, and environmental considerations. The highly fragmented nature of the Asian market further complicates navigation.

Despite obstacles, optimism prevails. Investors and operators are adapting to diverse regulatory landscapes, with a focus on offering products and services across multiple markets. China and Singapore, two key players, are easing data controls and lifting moratoriums, albeit selectively, showcasing the ongoing evolution of the regulatory environment.

As data centers strive to meet escalating demands, issues such as cooling system improvements take center stage. Increased use of graphics processing units (GPUs) to handle complex AI computations raises power consumption and heat emission concerns.

In the face of evolving risks and regulations, Glen Duncan, Asia-Pacific Director of Data Center Research at Jones Lang LaSalle, underscores the importance of staying informed. Investors and operators must remain vigilant and adaptive to navigate the dynamic landscape, where government regulations around data privacy, national data sovereignty, and sustainability continue to evolve across diverse markets in Asia.

How can investors capitalize on the Asian data center boom?

Investors can invest through several avenues:

1. Real Estate Investment Trusts (REITs): Look for REITs specializing in data center properties in the Asia-Pacific region. Investing in these trusts allows individuals to gain exposure to the growing demand for data centers without directly owning the physical assets. Example: Equinix

2. Technology and Infrastructure Funds: Consider investing in mutual funds or exchange-traded funds (ETFs) focused on technology and infrastructure. These funds often include companies involved in data center development and operation. Example: Global X Data Center REITs & Digital Infrastructure ETF

3. Individual Stocks: Identify publicly traded companies in the data center industry with a strong presence in Asia. Key players include those involved in designing, building, and managing data centers, as well as cloud service providers experiencing significant growth. Examples: PLDT, Singapore Telecommunications

Remember that investing always carries risks, and thorough research is essential before making any financial decisions. Additionally, understanding the specific dynamics of the data center market in Asia, including regulatory considerations and geopolitical factors, is crucial for making informed investment choices.